If you’re living with a disability, planning for your financial future can feel overwhelming.

The Registered Disability Savings Plan (RDSP) is a powerful tool designed specifically to help you save for long-term financial security, with significant support from the Canadian government.

Here’s how it works and why it might be right for you.

What is an RDSP?

An RDSP is a savings plan created to help people with disabilities save for the future.

It’s not just about putting money aside—it’s about growing your savings with tax-free investment income and government contributions that can multiply what you save.

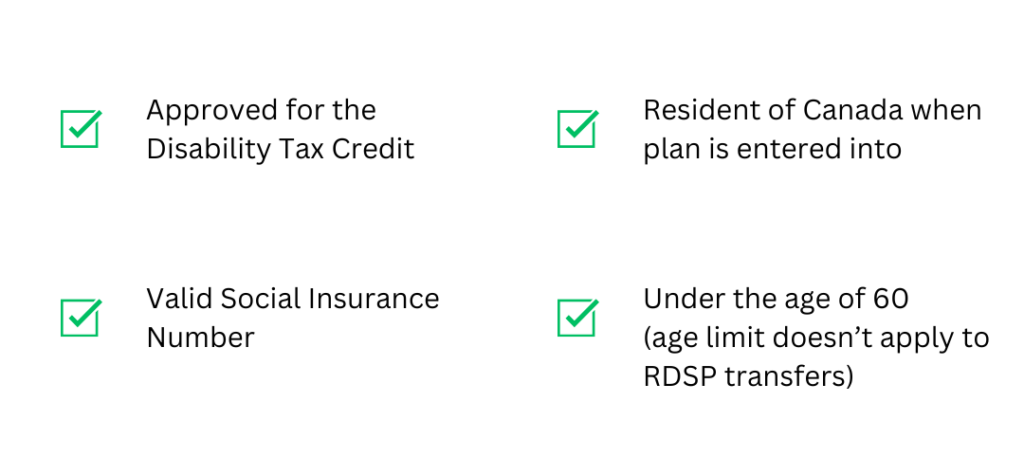

An RDSP is available to individuals who meet specific criteria:

For example, Sarah, a 30-year-old living with a disability, is eligible and can use an RDSP to save for future care and living expenses.

The plan can be opened by the beneficiary themselves if they are mentally capable, or by a legal guardian, parent, or qualifying family member if they are not.

How do RDSP grants work?

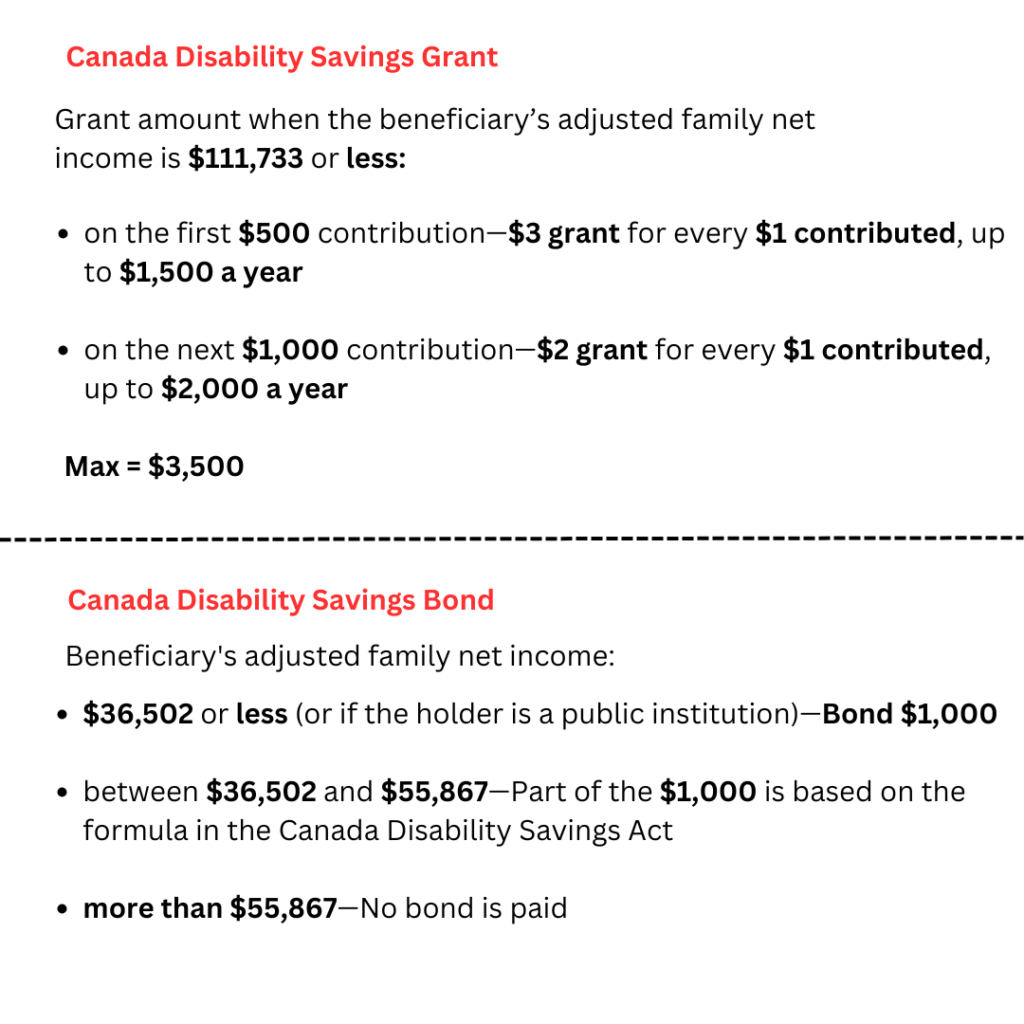

Contributions to the plan are not tax-deductible, but the investments grow tax-free. Moreover, the government boosts savings through the Canada Disability Savings Grant (CDSG), which matches contributions by up to 300%. Also, the Canada Disability Savings Bond (CDSB) provides up to $1,000 annually for low-income families, even without contributions.

For instance, if Sarah contributes $1,000 to her RDSP, she could receive a maximum of $3,500 in grants and bonds for the year and $70,000 in her lifetime.

How can I withdraw from my RDSP?

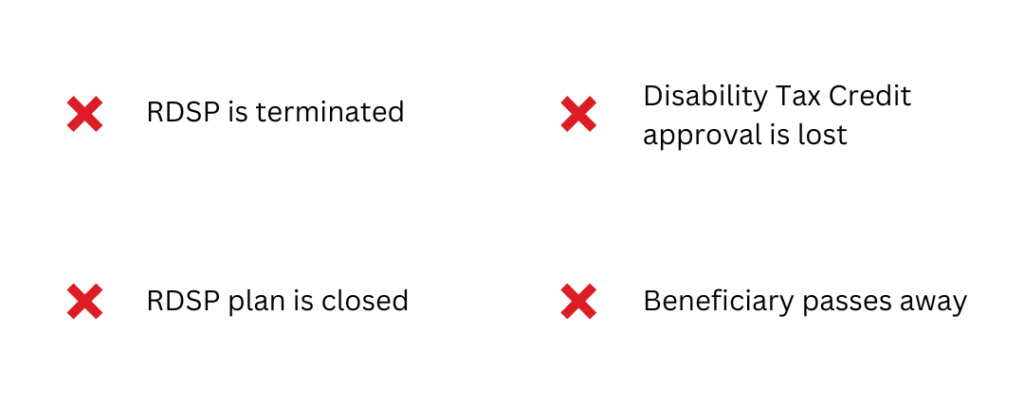

Withdrawing from an RDSP can provide much-needed funds, but it’s essential to understand the repayment rules tied to government contributions.

The 10-year repayment rule requires all grants and bonds contributed in the last 10 years to be repaid if any of the following conditions are met:

For regular withdrawals, the proportional repayment rule applies, requiring $3 of grants and bonds to be repaid for every $1 withdrawn, up to the assistance holdback amount.

For example, Sarah received $20,000 in government grants and bonds over the last 10 years and decided to withdraw $1,000 to cover medical expenses.

Under the proportional repayment rule, she would need to repay $3,000 (three times the withdrawal amount) to the government, reducing her assistance holdback amount to $17,000 while allowing her RDSP to continue growing.

If Sarah’s condition worsens and her life expectancy is less than five years, she could withdraw up to $10,000 annually without triggering the 10-year repayment rule, provided her plan is designated as a Specified Disability Savings Plan (SDSP).

These rules ensure RDSP funds are preserved for long-term needs while offering flexibility for emergencies, making it vital to plan withdrawals carefully and consult with your RDSP issuer for guidance.

How can I get started with an RDSP plan?

To learn how an RDSP can help you or a loved one achieve long-term financial security, schedule an online consultationor reach out through the Contact Us page. Get personalized advice on eligibility, government contributions, and withdrawal strategies to make the most of this powerful savings tool.