The Messi: Protecting What You Built

With the 2026 World Cup in North America, there’s no shortage of debate about who the greatest of all time really is.

But here’s what I find more interesting than the GOAT debate: Messi, Ronaldo, and Mbappe each represent a completely different stage of a career. Over the next three posts, we’re going to break down what each of them can teach Canadian business owners about building, protecting, and passing on wealth.

We’re starting with Messi, because his stage is the one with the highest stakes and the least room for error.

Messi isn’t chasing records anymore. He’s in Miami, playing on his terms, doing exactly what he wants, when he wants. The work of building a legacy is done. What’s left is making sure it actually lasts.

That’s the mindset for business owners in the wealth protection stage. You’ve built something real. The business has generated meaningful retained earnings. The priority isn’t growth anymore, it’s protection.

The Problem Nobody Talks About

Here’s what surprises most business owners when I bring it up: your corporation doesn’t disappear when you do.

If you’ve spent years building retained earnings inside your company, that money is still sitting there on the day you pass away. And without a plan, it gets hit with tax not once, but potentially twice, first as a deemed disposition of your shares, then again when the money is eventually paid out to your estate.

I’ve sat across from business owners who had no idea that a significant portion of what they built over 20 or 30 years was going to disappear to taxes simply because nobody had structured a plan to move that wealth out efficiently.

This isn’t a hypothetical. It’s the default outcome for any corporation with retained earnings and no structure in place.

The corporation doesn’t retire when you do. Without a plan, neither does the tax exposure.

Corporate Life Insurance and the Capital Dividend Account

This is where corporate-owned life insurance becomes one of the most powerful tools available to business owners in this stage.

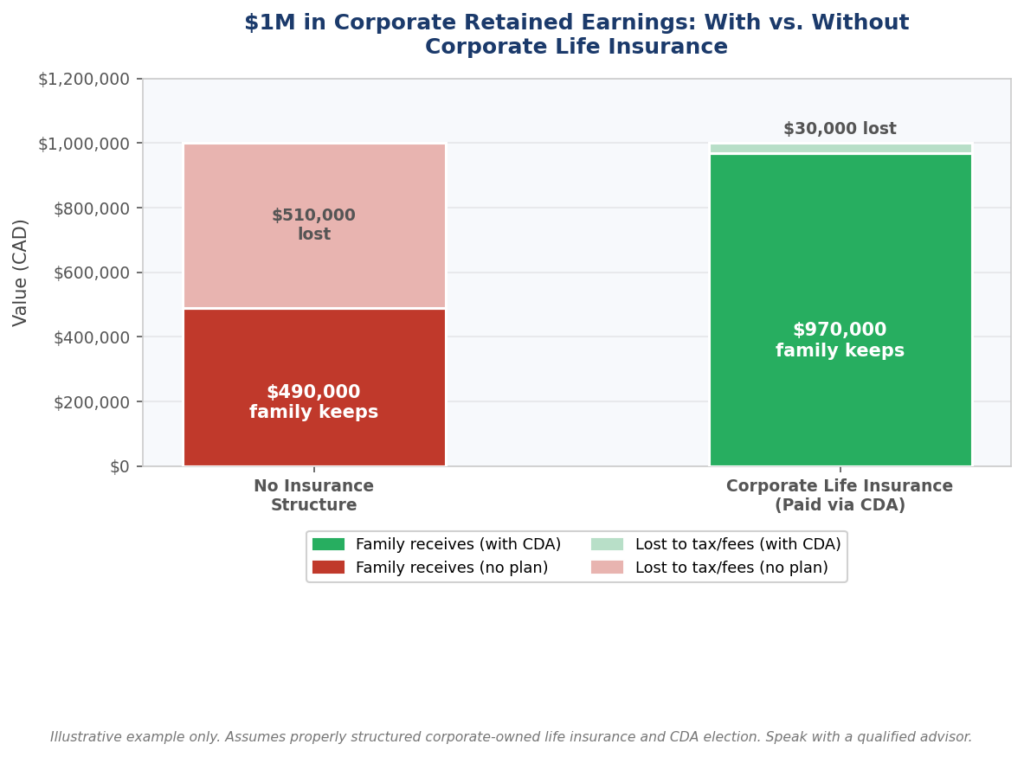

When a corporation owns a life insurance policy on you, the death benefit is paid to the company tax-free. A large portion of that benefit then gets credited to something called the Capital Dividend Account, or CDA. Money paid out of the CDA to your estate or your beneficiaries flows out completely tax-free.

In practice, this means a properly structured policy can move a significant amount of wealth out of your corporation without the tax drag that would otherwise apply. The chart below shows what this looks like with $1M in retained earnings.

The difference isn’t small. Without a plan, more than half of that value can be lost to tax. With the right structure, the vast majority reaches your family.

This is also why timing matters. Life insurance gets more expensive, and harder to qualify for, as you get older or if your health changes. The best window to put this in place is well before you think you need it.

Holdco Structures: Separating What’s at Risk from What’s Protected

The second piece that often gets overlooked is the structure itself. If your retained earnings are sitting inside your operating company, they’re exposed to the same risks as the business: lawsuits, creditors, and operational liabilities.

A holding company structure separates your accumulated wealth from your day-to-day operating risk. Profits can move from the operating company to the holdco, generally on a tax-deferred basis, and from there they’re protected and can be invested or structured independently of what’s happening in the business.

For owners in the protection stage, this isn’t optional. If you’ve built meaningful retained earnings and they’re still sitting exposed inside your opco, that’s one of the first things worth fixing.

Estate Freeze: Locking In Today’s Value

The third tool, and one of the most strategic for this stage, is the estate freeze.

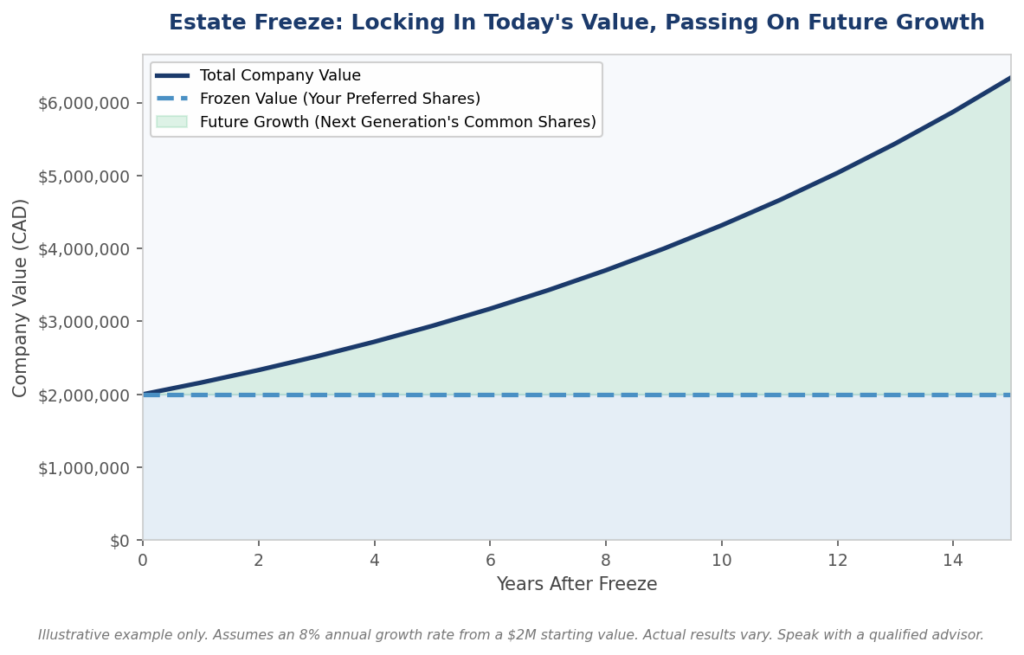

An estate freeze allows you to lock in the current value of your company in exchange for fixed-value preferred shares, while new common shares, which capture all future growth, are issued to your children or a family trust.

The benefit is twofold. First, it caps your personal tax liability at today’s value rather than at some future, larger number. Second, it allows the next generation to start benefiting from the company’s growth immediately, often without triggering tax until those shares are eventually sold or the company is wound down.

As the chart shows, the gap between your frozen value and the company’s total value only grows over time. Every year you wait to implement a freeze is a year more growth gets added to your personal tax exposure instead of being captured by the next generation.

An estate freeze doesn’t give away the company. It separates what you’ve already earned from what’s still to come.

Where This Leaves You

If you’re in the wealth protection stage, here’s a useful way to think about it: every dollar still sitting inside your corporation without a plan is a dollar that’s exposed. The longer it sits there unprotected, the more there is to lose.

A few questions worth asking yourself:

- Do you know how much of your retained earnings would actually reach your family if something happened to you tomorrow?

- Is your wealth sitting inside your operating company, exposed to business risk, or has it been moved to a protected holdco structure?

- Have you looked at whether an estate freeze makes sense for your situation?

- Do you have corporate life insurance in place, structured to take advantage of the Capital Dividend Account?

If any of those feel uncertain, that’s exactly where the conversation should start.

Next up in this series: The Ronaldo, what it means to be in your peak earning years, and how to make sure you’re capturing everything that window has to offer.

If you want to talk through your own situation and what the protection stage looks like for your business, Book a book an online consultation or reach out to our team.