Most incorporated owners have a compensation plan. Very few have a compensation strategy.

Kevin O’Leary has a line that sticks with me: “Every dollar is a soldier. You need to know where it is and what battle it’s fighting.”

He’s talking about investing. But every time I sit down with a Canadian business owner, I think about that line for a completely different reason.

Because here’s what I keep seeing: incorporated business owners who have built something real, who are generating solid revenue, who are reinvesting everything back into the company, and who, when I ask them what they’re actually paying themselves, give me a number that doesn’t add up.

Not because they’re struggling. But because nobody has ever shown them the full picture.

The “I’ll Pay Myself Later” Trap

It usually starts with good intentions. You incorporate. The accountant says leaving money in the corporation has tax advantages. So you do. You take a modest salary, keep your personal draw low, and tell yourself you’ll figure out the rest later.

Later never comes. Or when it does, it arrives with a whole new set of problems.

The issue isn’t that you’re leaving money in the corporation. That can absolutely be a smart strategy. The issue is when there’s no plan attached to it. No structure. No intentional decision about what that retained earnings is actually doing for you, your family, or your retirement.

A salary without a plan is just an expense. A compensation strategy is an asset.

What a Compensation Strategy Actually Looks Like

When I work with business owners on this, we’re not just talking about a number on a T4. We’re building a structure. That structure usually involves a few key pieces:

Salary vs. Dividends: the split between these two matters more than most people realize. Salary creates RRSP room and pensionable earnings. Dividends can be more tax-efficient in the right circumstances. The right mix depends on your income level, your spouse’s situation, and your goals.

Individual Pension Plans (IPPs): if you’re over 40, an IPP can let you shelter significantly more than an RRSP. It’s one of the most underused tools available to incorporated owners, and it benefits from being set up sooner rather than later.

Corporate Retained Earnings: money sitting inside your corporation isn’t automatically working for you. It needs to be invested or structured in a way that serves a purpose, whether that’s growth, passive income, or a future exit.

Life Insurance as a Corporate Asset: properly structured corporate-owned life insurance can be one of the most efficient ways to move wealth out of a corporation tax-efficiently. This is where the strategy goes from good to exceptional.

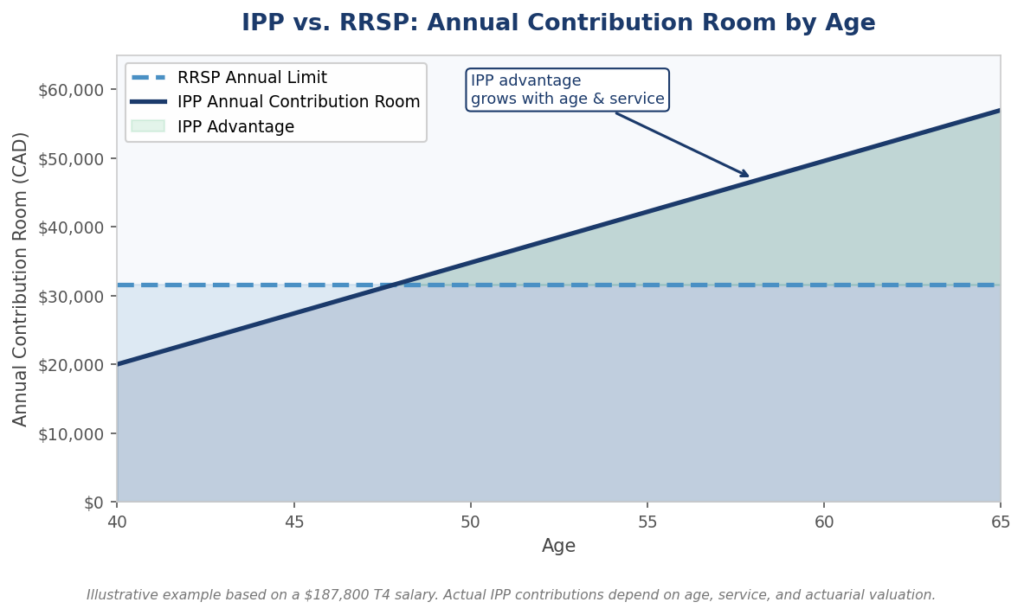

IPP vs. RRSP: Why the Gap Matters as You Get Older

One of the most common reactions I get when I explain IPPs is: “Why hasn’t anyone told me about this before?”

The short answer: most advisors aren’t set up to recommend them. They’re more complex to administer than an RRSP, and the benefit grows significantly with age. But for an incorporated owner over 40, the difference in annual contribution room can be substantial, and it compounds.

As the chart above shows, an IPP’s contribution room grows with your age and years of service. By your mid-50s, you could be sheltering nearly double what an RRSP allows. That gap represents real money, tax-deferred, compounding inside a structure that’s also creditor-protected.

The Real Cost of Doing Nothing

Here’s what most people don’t consider: every year you delay building this structure is a year you’re not compounding it.

O’Leary would call this “soldiers sitting in the barracks.” Your money is there. It’s just not working.

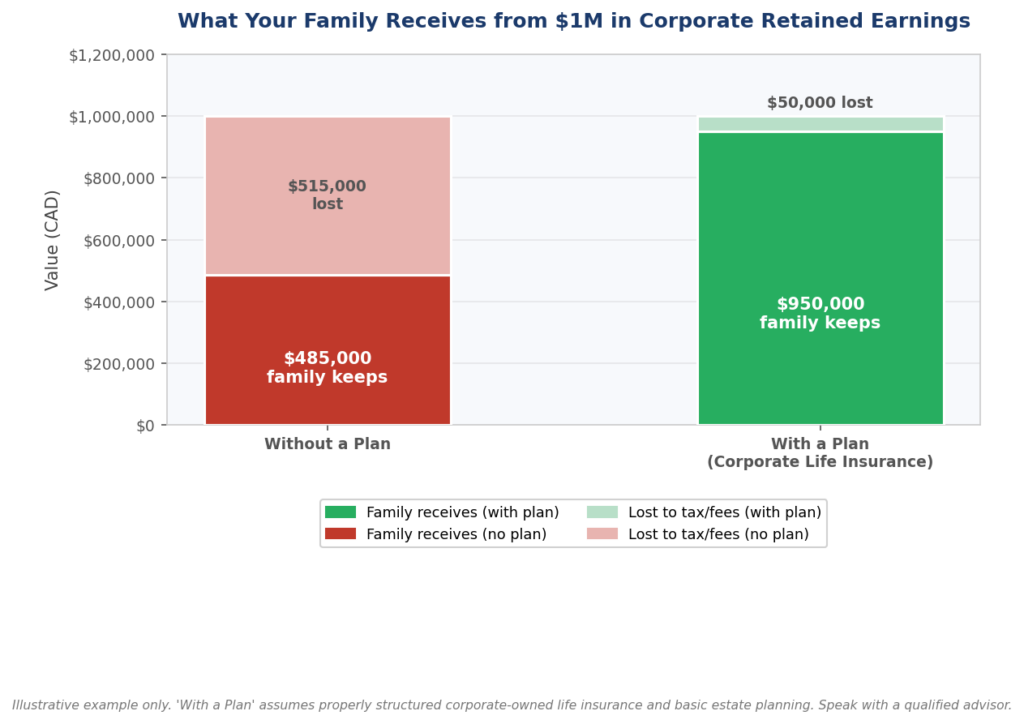

More importantly, without a compensation strategy, you’re also exposed. If something happened to you tomorrow, disability, illness, death, what does your family or your business actually have to fall back on? A corporation with retained earnings and no plan in place can create enormous tax headaches for your estate.

Without a plan, over half of what you’ve built inside your corporation can disappear before it reaches your family. Life insurance held corporately is one of the most powerful tools to fix this because the death benefit flows out through the Capital Dividend Account, minus the cost adjusted basis.

I’ve had conversations with business owners who didn’t realize that a significant portion of what they’d built over 20 years was going to disappear to taxes because there was no structure in place to protect it.

The goal isn’t just to build wealth inside your business. It’s to make sure that wealth actually reaches you and your family.

Where to Start

This doesn’t have to be complicated. The first conversation is usually the most important one, and it’s not about selling you anything. It’s about understanding where you are and what you’re actually trying to accomplish.

A few questions worth asking yourself:

Do you know the optimal salary/dividend split for your current income level?

Have you looked at whether an IPP makes sense for you?

Do you have a plan for your retained earnings beyond leaving it in the company?

Is your corporation structured in a way that protects your family if something happens to you?

If any of those feel uncertain, that’s a good starting point.

If you want to talk through your compensation structure and what options might make sense for your situation, I’m always happy to start that conversation. Book an online consultation or reach out to our team.