Cristiano Ronaldo and the Discipline of Peak Years

In Part 1 of this series, we talked about Messi and what it means to protect what you’ve already built. Now we’re moving to a different stage entirely.

Cristiano Ronaldo is 41 years old and still playing at the highest level, still scoring, still chasing records most players half his age will never touch. What separates him isn’t just talent. It’s discipline. Every training session, every recovery routine, every decision is built around extracting the absolute maximum from the years he has left at the top.

That’s the mindset for business owners in their peak earning years, typically mid-40s through late-50s. The business is established. Revenue is strong. But the window to capitalize on it is finite, and most owners aren’t structured to capture everything that window offers.

The Problem: Good Years, Incomplete Structure

Here’s what I see most often with owners in this stage. The business is doing well. They’re taking a reasonable salary. They’re contributing to an RRSP. On paper, it looks fine.

But fine isn’t the same as optimized. Most owners in their peak years are leaving meaningful value on the table simply because nobody has shown them what else is available.

Two things in particular tend to be missing: a properly structured Individual Pension Plan, and a deliberate plan for retained earnings instead of letting them sit idle in the corporation.

Peak earning years are finite. What you do with them doesn’t have to be.

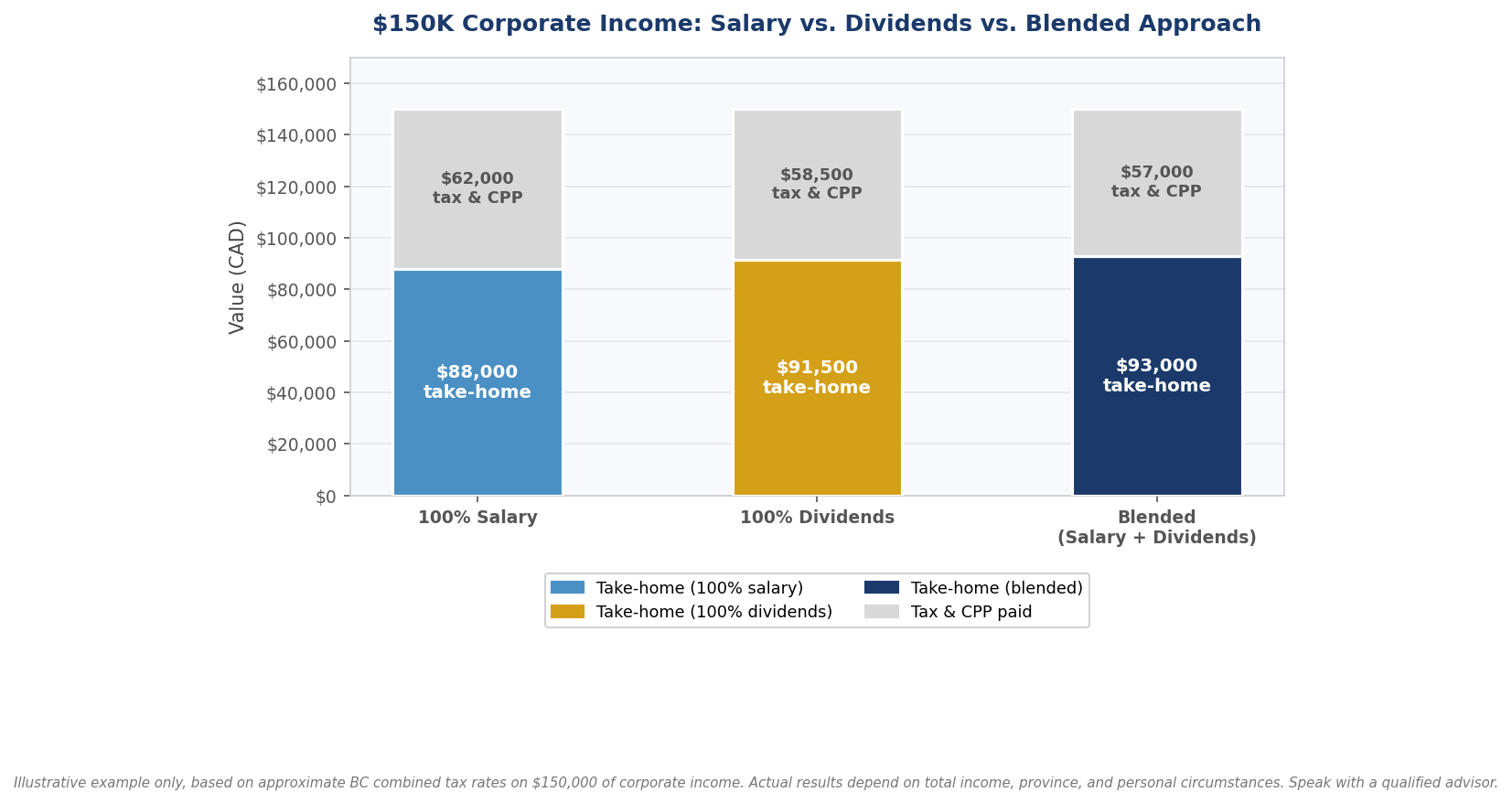

Salary vs. Dividends: The Mix Most Owners Get Wrong

If you’re over 40 and incorporated, how you pay yourself matters more than most owners realize.

Salary and dividends are taxed differently, and they trigger different downstream effects. Salary is deductible to the corporation and creates RRSP room and CPP contributions, but it’s taxed at your full personal rate and comes with payroll costs. Dividends avoid CPP and payroll tax, but they don’t create RRSP room and they’re taxed differently depending on whether they’re eligible or non-eligible dividends.

Most owners default to one extreme or just take whatever their accountant set up years ago. Neither is usually the optimal mix.

As the chart shows, a blended approach can outperform either extreme. The right mix depends on your total income, your province, whether you have a spouse you can income-split with, and how much RRSP or pension room you actually want to build.

This isn’t a set-it-and-forget-it decision either. As your income grows or the rules change, the optimal split shifts. Reviewing it annually, rather than leaving it on autopilot, is often where the biggest gains are found.

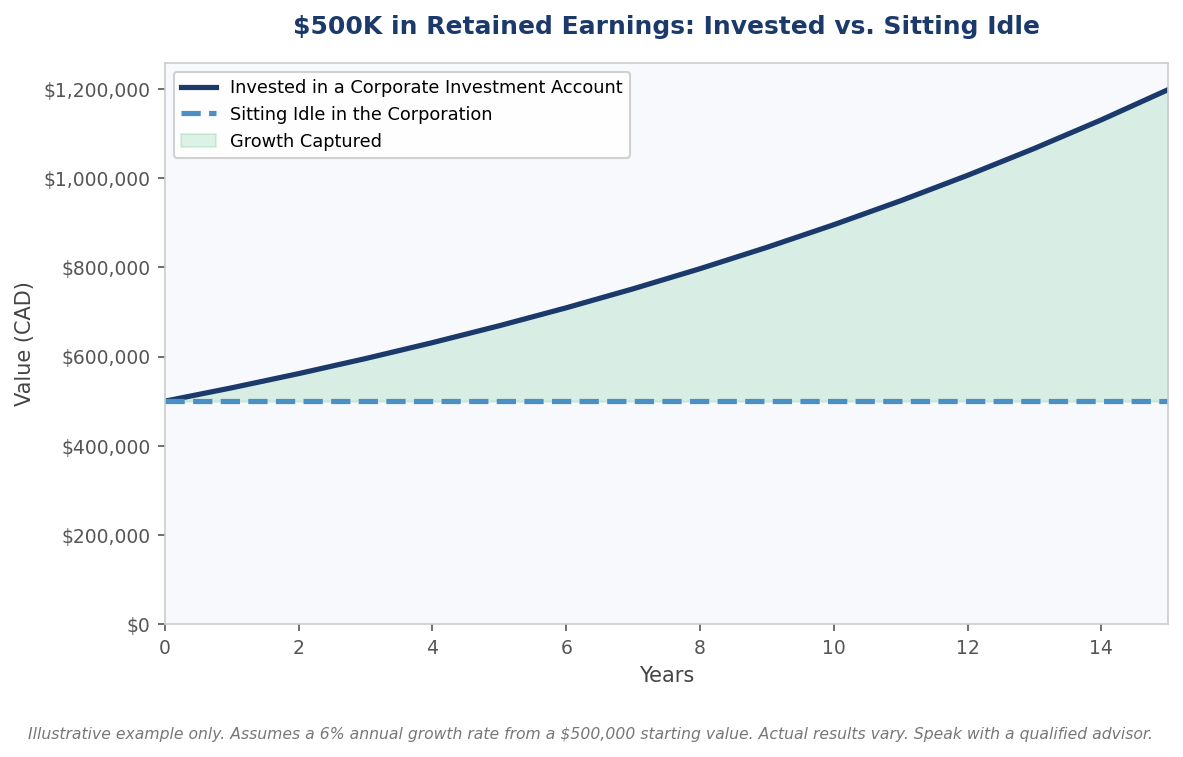

Retained Earnings: Working Capital, Not Dead Capital

The second piece is what happens to the money that stays inside the corporation.

For a lot of owners, retained earnings just sit. It’s not earmarked for anything specific, it’s not invested, it’s just there as a cushion. That instinct makes sense, but it’s also expensive. Cash sitting idle in a corporate account isn’t compounding. It’s not doing anything except slowly losing value to inflation.

A corporate investment account changes that. Retained earnings can be invested in a portfolio appropriate for the corporation’s time horizon and risk tolerance, and from that point forward, the money is actually working.

The chart makes the case clearly. Fifteen years of sitting idle versus fifteen years of compounding growth is not a small difference, it’s hundreds of thousands of dollars. The earlier this gets set up, the larger that gap becomes.

There are tax considerations that come with investment income inside a corporation, including how passive income interacts with the small business deduction. This is exactly why the structure matters as much as the decision to invest in the first place.

Idle capital isn’t safe capital. It’s capital that’s quietly losing ground every year.

Where This Leaves You

If you’re in your peak earning years, the question isn’t whether the business is doing well. It’s whether your personal and corporate financial structure is keeping pace with it.

A few questions worth asking yourself:

- Have you reviewed your salary and dividend mix in the last few years as your income has changed?

- Have you looked at whether an IPP makes sense alongside your current compensation structure?

- Do you have key person insurance in place in case something interrupts your ability to run the business during these critical years?

If any of those feel uncertain, that’s exactly where this conversation should start.

Next up in this series: The Mbappe, what it means to build the right foundation early, before you need it.

If you want to talk through what your peak earning years should look like structurally, book an online consultation or reach out to our team.